MPF Ordinance in Hong Kong

This tutorial explains the core concepts of MPF Ordinance in Hong Kong. All data were updated as at 2015 March, I may not be able to constantly update the Ordinance.

MPF Enrollment

Permitted Period is the period within which an employer must enroll employees in an MPF scheme.

| Employment type | Permitted Period |

| Non casual employee | the first 60 days of employment |

| Casual employee | the first 10 days of employment |

| Self employed person | the first 60 days of employment |

Self employed persons are required to enroll themselves to become members of MPF schemes regardless of their level of income (they must enroll even if they do not need to contribute), unless they are exempt persons.

Except persons include domestic employee, a self employed hawker etc.

MPF Contribution Amount

The below tables shows MPF contribution for employee, employer and self employed person. Note the following effective dates.

– Minimum relevant income of $7,100 per month effective 1 November 2013

– Maximum relevant income level of $30,000 per month effective 1 June 2014

Monthly paid employee

| Monthly Relevant Income | Employee Contribution | Employer Contribution |

| Below $7100 | none | 5% |

| >=$7100 to $30000 | 5% | 5% |

| >$30000 | $1,500 | $1,500 |

| Daily Relevant Income | Employee Contribution | Employer Contribution |

| Below $280 | none | $10 |

| >=$280 to <$350 | $15 | $15 |

| >=$350 to <$450 | $20 | $20 |

| >=$450 to <$550 | $25 | $25 |

| >=$550 to <$650 | $30 | $30 |

| >=$650 to <$750 | $35 | $35 |

| >=$750 to <$850 | $40 | $40 |

| >=$850 to <$950 | $45 | $45 |

| >=$950 | $50 | $50 |

Self employed person

Self employed persons can choose to make mandatory contributions on a monthly or yearly basis.

Monthly Basis

| Monthly Relevant Income | Employee Contribution | Employer Contribution |

| Below $7100 | none | 5% |

| >=$7100 to $30000 | 5% | 5% |

| >$30000 | $1,500 | $1,500 |

| Yearly Relevant Income | Employee Contribution | Employer Contribution |

| Below $85200 ($7100*12) | none | 5% |

| >=$85200 to $360000 | 5% | 5% |

| >$360000 ($30000*12) | $18000 ($1500*12) | $18000 |

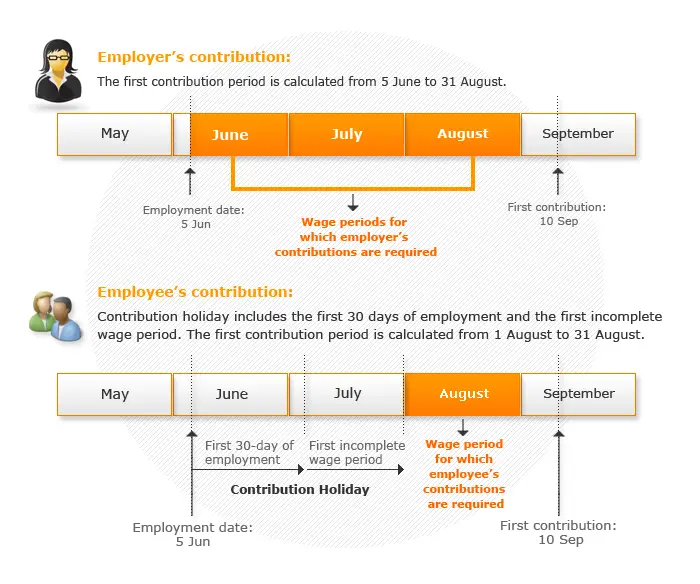

First contribution day

Contribution Period refers to each period for which the employer pays or should pay relevant income to the employee.

Wage Period refers to each period for which the employer pays or should pay relevant income to the employee.

Contribution Holiday is the exemption period where employee does not need to contribute MPF, it is the first 30 days of employment plus the incomplete wage period that immediately follows the 30 day period.

| Employee type | Deadline of first contribution | Contribution Period |

| Monthly wage | 10th day of the following month after Contribution Holiday | Employer Contribution: From the first day of employment plus 1 month after Contribution Holiday Employee Contrition: The first Wage Period after Contribution Holiday |

| Daily wage | Next working day after pay day or within 10 days after contribution period |

From the first day of employment |

Tax Deduction

For employee

| Contribution | Tax Deduction |

| Employee Mandatory Contribution | Subject to the maximum deduction amount prescribed in IRD for that year (in fact the max deduction amount = max contribution*12) |

| Employee Voluntary Contribution | Non-deductible |

| Employer Contribution | Non-deductible |

For employer

– Employer contribution of MPF and ORSO are tax deductible up to 15% of the total annual emoluments of the employees

– Voluntary contribution made by employer are subject to tax

Involuntary Termination

Employer can offset employees’ severance payment (遣散費) or long service payment (長期服務金) with the accrued benefits derived from employer’s contribution.

After employer pays SP or LSP to employee, employer can apply to the MPF trustee with supporting evidence for re-payment of the relevant amount from the employee’s accrued benefits derived from employer’s contributions.

Withdrawal of Accrued Benefits

Normally, employee can withdraw the accrued benefits on age 65. But you can withdraw earlier in the following situations

| Reason for Early Withdrawal | Description | Supporting documents |

| Early retirement | You must be at least 60 years old and declare that you have permanently ceased your employment or self-employment. You can be employed again but need to enroll MPF scheme. | 1) Identity document (e.g. HK ID Card) 2) Claim form for payment of accrued benefits [MPF(S) – W] 3) Statutory declaration form [MPF(S) – W(SD1)] |

| Permanent departure from Hong Kong | You must declare that you have departed or are about to depart from Hong Kong permanently, and provide proof satisfying the trustee that you are permitted to reside permanently in a place outside Hong Kong. This reason for early withdrawal can only be used once in a lifetime. | 1) Identity document (e.g. HK ID Card) 2) Claim form for payment of accrued benefits [MPF(S) – W] 3) Statutory declaration form [MPF(S) – W(SD2)] 4) Documentary proof satisfying the trustee that you are permitted to reside permanently at a place outside Hong Kong |

| Total incapacity | You are eligible if you have become permanently unfit to perform the particular kind of work you were doing in your previous job. You must provide a medical certificate issued by a registered medical practitioner or registered Chinese medicine practitioner certifying such condition and a letter issued by your former employer showing your termination of employment. | 1) Identity document (e.g. HK ID Card) 2) Claim form for payment of accrued benefits [MPF(S) – W] 3) Letter issued by your former employer certifying your termination of employment (If you were not employed immediately before becoming totally incapacitated and (a) is unable to obtain the letter from your former employer or (b) has been unemployed for more than 7 years, you can instead submit the statutory declaration form [MPF(S) – W(SD4)] 4)“Certificate of a person’s permanent unfitness for a particular kind of work” form [MPF(S) – W(M)] |

| Small balance account. | You must have only one MPF account with a balance of not more than $5,000, and the period between the date of your claim and your last contribution date has exceeded at least 12 months, and you declare that you do not expect to become employed or self-employed in the foreseeable future. | 1) Identity document (e.g. HK ID Card) 2) Claim form for payment of accrued benefits [MPF(S) – W] 3) Statutory declaration form [MPF(S) – W(SD3)] |

| Death | The accrued benefits of a deceased member are a part of the member’s estate and therefore must be claimed by the scheme member’s personal representative or the Official Administrator. | 1) Identity document of the personal representative (e.g. HK ID Card) 2) Claim form for payment of accrued benefits [MPF(S) – W] 3) Letter of Administration or Probate |

Click here to download the Forms

References

https://www.peak.edu.hk/cpdc/en/pdf/Eng_Study_Notes_Jun_2014.pdf